Single Americans would rather buy a home than pay for a wedding, survey finds

Unmarried Americans are prioritizing homeownership over paying for a wedding, according to a new survey. (iStock)

Some of life's biggest milestones, like getting married and buying a home, are also life's most significant financial commitments. So when asked to decide between the two, a new survey showed that many singles are choosing to buy a home rather than have a wedding.

About 4 in 5 unmarried Americans (82%) said they would rather invest in a home than pay for a big, expensive wedding, according to a new survey from Coldwell Banker Real Estate. That number is even higher among single women, at 85%.

Despite a competitive housing market, prospective buyers are still committed to homeownership, according to Coldwell Banker President and CEO M. Ryan Gorman. And he doesn't expect this trend to slow down anytime soon.

"The 2021 housing market has been marked by low inventory and competition as Americans continue to keep homeownership top of mind," Gorman said. "Our latest survey suggests that, with generations of all ages and backgrounds prioritizing homeownership over other financial goals, this sellers' market may continue into 2022."

Keep reading to learn more about homeownership and weddings, including tips on how to finance each. Then, visit Credible to compare interest rates on a variety of financial products, such as mortgages and wedding loans.

WHAT ARE PROPERTY TAXES? A GUIDE FOR FIRST-TIME HOME BUYERS

Homeownership or a wedding? You may not have to choose

A typical wedding costs nearly $30,000, according to the 2020 Brides American Wedding Study. Such a large amount of money may make it difficult for couples to also be able to afford a down payment on a home, prompting them to choose between the two.

But since interest rates are currently low on a variety of financial products, it may be possible to both buy a home and pay for a wedding.

35% OF MILLENNIALS SAY STUDENT LOAN DEBT IS PREVENTING THEM FROM BUYING A HOME

Mortgage rates remain historically low, making it a good time to buy a home

High demand from homebuyers paired with low housing inventory is driving competition in today's housing market, causing home values to soar. But despite rising home prices, now is a good time to buy a home, thanks to historically low mortgage rates.

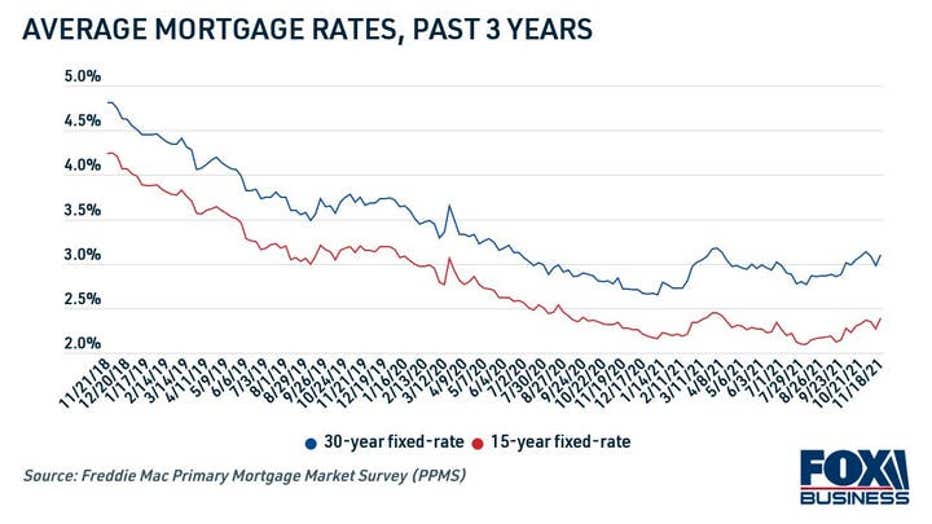

Over the past 3 years, the average rate on a 30-year fixed-rate mortgage has fallen from nearly 5% to around 3%, according to data from Freddie Mac. This makes the cost of borrowing a home loan much more affordable in the long term. Plus, lower rates typically mean lower mortgage payments.

ARE MORTGAGE CLOSING COSTS AN ELIGIBLE TAX DEDUCTION?

But interest rates can't stay this low forever. The Federal Reserve projects a rate hike as early as 2022, which will inevitably cause mortgage interest rates to spike. And experts also agree, with the Mortgage Bankers Association (MBA) predicting that mortgage rates will average 4.0% in 2022 and 4.3% in 2023.

The time to lock in a low interest rate on a home loan is running out. If you're considering buying a home, get prequalified for a mortgage on Credible for free. You can compare rates from top mortgage lenders, all without impacting your credit score.

JOINT TENANCY VS EQUAL OWNERSHIP: WHAT TO KNOW ABOUT A SHARED HOME

New borrowing options make it easier to pay for a wedding

Marriage isn't a prerequisite for buying a home, but couples may still consider tying the knot before becoming joint homeowners. If you plan on having your (wedding) cake and eating it, too, then it may be possible to finance your big day with a wedding loan. This is simply a type of unsecured personal loan that's used to pay for wedding expenses like the ceremony and reception — or even a honeymoon.

Since personal loans don't require collateral, the funds can be used however you see fit. Personal loans are disbursed directly into your bank account in a lump sum of cash, and they're repaid in fixed monthly installments over a set period of time, typically a few years.

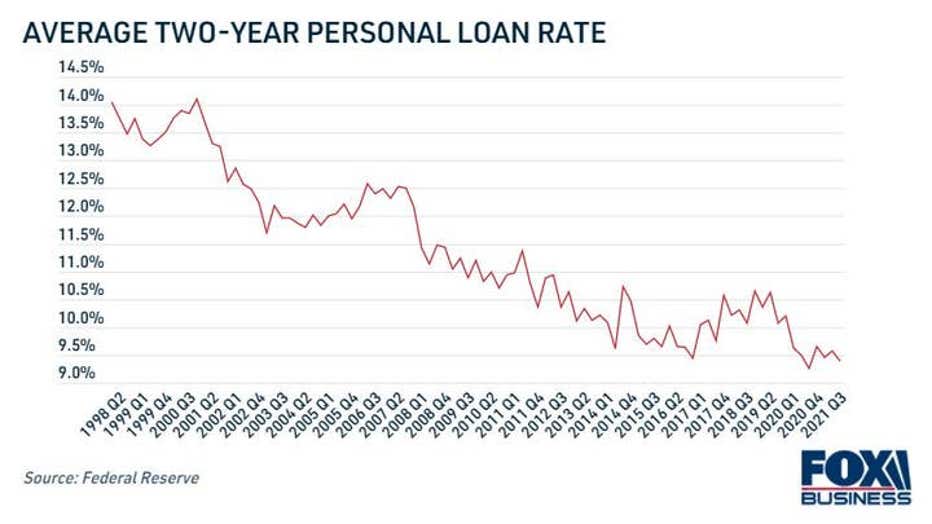

Personal loan interest rates are near all-time lows, according to the Federal Reserve, making these loans a cheaper wedding financing option than ever before.

Keep in mind that it's not typically advised to borrow money for unnecessary expenses, and that includes a big wedding. You'll have to pay interest on the loan, which increases the overall cost of hosting a wedding. Instead, you could save up in advance for your big day, even if that means postponing for a few years while you budget for the costs.

If you decide to borrow a personal loan for wedding expenses, it's important to compare rates across multiple lenders to ensure you're getting the lowest rate possible for your financial situation. You can browse personal loan offers tailored to you with a soft credit check on Credible. Then, use a personal loan calculator to estimate your monthly payments, fees and other repayment terms.

BEST PERSONAL LOANS FOR BORROWERS WITH A COSIGNER

Have a finance-related question, but don't know who to ask? Email The Credible Money Expert at moneyexpert@credible.com and your question might be answered by Credible in our Money Expert column.